The Supply Chain Dillema: Save for a Crisis? Or Invest for Future Resilience?

At FINAT’s European Label Forum 2023 held last June, Prof. Bram DeSmet explored the current state of the extended label supply chain. On the occasion of his previous appearance at the ELF in Baveno last year, most companies were facing the same challenge, namely a shortage of components and raw materials, leading to delivery problems towards their customers. Where are we now, the year after? We asked Bram to share his takeaways from the pre-conference interviews and workshop in Vienna this year.

This year, the supply chain problems were more nuanced. Except for specific categories like micro-electronics, the label supply chains now seemed more confronted with an excess of inventory and a lack of demand. We all bought too much product when product was short. Next to a slowing demand because of economic uncertainty, we are further slowing the demand because of inventory build-offs.

When asked the question 'Will markets return back to normal or should we prepare for continued volatility?', most of the participants tended to agree or strongly agree with the latter. This places us for a dillemma. Should we now save on costs and cash (inventories) in the supply chain to prepare for a potential economic crisis? Or should we invest in making our supply chains more resilient and more agile, to prepare for future disruptions?

Based on intake interviews with different stakeholders from different steps in the supply chain, I introduced 4 possible pillars to improve our supply chain resilience and increase our agility.

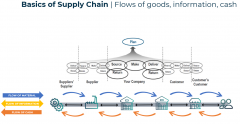

The basics of supply chain management

The basis of supply chain management is simple. It is about moving goods from the suppliers' supplier all the way down to the customers' customer. There is a physical flow of goods and an inverse flow of information and cash. We place orders on each other and pay each other.

Improving the resilience and agility in the supply chain will depend on 2 main drivers: collaboration in the supply chain, and the digitalization of the information and cash flows.

Roundtables: 4 key topics

After my initial keynote presentation, introducing the above topics, we organized roundtable discussion to explore what are key opportunities and what are key hurdles for the sector to improve collaboration with key customers, with key suppliers, and the so-called ‘horizontal collaboration’ with competitors. A fourth topic was the digitalization of the extended label supply chains.

Connecting our disconnected systems: collaboration and digitalisation

Across the different levels of the chain, visibility and transparency are key. Visibility on stocks, visibility on consumption, visibility on forecasts. Out of the roundtables it became clear we can work with customers on creating more flexibility by having more and faster approval of alternatives. There is a lot of value to be created by educating customers on the best opportunities and options. We don't fully leverage each others' expertise. Comparable options hold at the supplier side. Do we give visibility to our suppliers? Do we ask for the best options or do we just negotiate on price? With competitors all of this is possible in the ‘non-competitive areas’. Where are we really competing and where are we not? Sharing information on excess paper inventories or spare parts for machines were named as easy options. Once the trust is there, digitalization can form the backbone of the improved collaboration. We talked about 'connecting our currently disconnected systems' as a general opportunity. When we do so it will allow the full chain to gain significantly in efficiency.

Hurdles

Collaboration and digitalization come with a lot of hurdles though. Do we really dare to choose key customers as an organization? Having a more intense collaboration may simply not be feasible with all customers. Even if we collaborate with key customers, we may still come to the conclusion that they too are in the dark on where their customers are going. On the supplier side we talked about the lack of alternatives. If the market of key raw materials is highly concentrated, we may simply lack the options to create suffient agility and resilience. And how do we create trust, and an equal give and take? That was most prominent in the discussion about collaboration with competitors but it applies to any type of collaboration. And how do we deal with confidentiality? That too surfaced in the discussion on collaboration with competitors but it applies to any type of collaboration. And how do we deal with the generational differences in our joined organizations? Younger people may be digitally savvy but have to learn how to build a trusted relationship. The less younger generations may be experts in building trusted relationships but have a hard time to trust and handle the powerful capabilities of recent technologies.

Mindset to make it work

In his conclusion, Bram was positively surprised. The label sector has a view to be relatively traditional and not advanced when it comes to supply chain management. On the one hand, yes, the sector is not a front-runner. If you look at the FMCG sector and how they collaborate with their key customers, the big retailers, they have defined and adopted processes many years ago. Another example is the automotive sector and how that collaborates with tier 1 and tier 2 suppliers. But the surprise came from the open mindset. When starting the discussion, I challenged the audience by stating ‘Don't bring me the excuses on why things are not going to work, but bring me the options on how we can make it work’. And that is exactly what this group has done. This is a sector that is entrepreneurial. We look for options and are willing to take a risk when exploring them. The sector has shown resilience in the COVID period by the mindset of its people. The key going forward will be to used that mindset to design structural solutions, so that as a sector we are better prepared for when the next disruption will hit us. Being more pro-active, more strategic, more advanced, not just in our digital printing and production technologies but also the supporting processes, will also be the best recipe to keep attracting bright young people and continue building the succesful future of this industry.